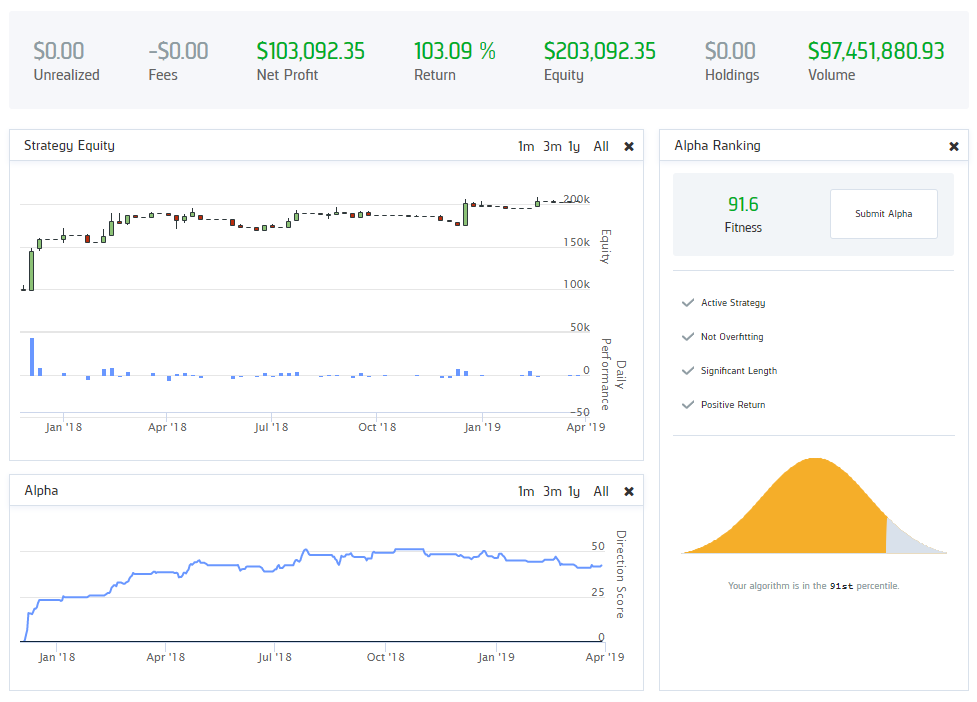

I’m going to begin with a bold statement: I believe the Laissez-Faire algorithm will be one of the best performing investment vehicles when compared to any other investment vehicle, commodity, index, bond, or ETF by the end of the next recession.

I know, it’s getting easy to get ‘cocky’ with the triple-digit performance this year of the algorithm, but I’d like to review the historical and statistical probabilities supporting this to create a more objective view of why it will likely outperform.

Nothing is certain in markets, and this is exaggerated in Bitcoin. What if the world’s major economies went into a sudden and violent recession? What if currencies began to hyper-inflate and destroy economic stability? Would Bitcoin really still be the thing that money is vested in? In my opinion, probably not. There is no doubt that the instability will create great amounts of volatility in markets, including Bitcoin, and that volatility will be catnip to Laissez-Faire.

In its design, the algorithm isn’t meant to be trend-dependent over when trading over a long period of time. While the performance is affected on short term-time frames, LF proves itself to do exactly as it was intended over longer periods of time. Laissez-Faire effectively reduces the overall volatility associated with holding Bitcoin while maximizing the upside gain. Holding Bitcoin from March 2019 (when the algorithm first began trading) is now equivalent in returns to the performance of the algorithm. Soon LF will likely be outperforming Bitcoin if the price continues to drop, which is comforting considering the volatile state of the market currently.

Volatility Based Performance Separate from Bitcoin’s Success

The point of Laissez-Faire is that its success isn’t contingent on the success of Bitcoin; so let’s analyze it’s performance during the bear markets of Bitcoin’s history and compare.

The most recent set of data to test this over is the bear market of 2018. I think it’s safe to say Bitcoin exited out of its year and a half long downtrend after getting back above 4250 in April of this year, 2019. Laissez-Faire unfortunately, wasn’t trading through this time, but this is where we introduce back-testing. Back-testing is 1:1 testing over historical data, so we can see exactly how LF would’ve performed over a certain period. The results are below, given LF started with $100,000 at the peak of Bitcoin prices in 2017 at $20,000 BTC/USD, and ending at $4000 BTC/USD.

So if we assume that a recession wouldn’t be good for Bitcoin, and it entered into another bear market comparable to 2018; we could assume a similar performance of Laissez-Faire over the same period shown below. The fact that Laissez-Faire is often not in a position for longer than a day, that it endures limited risk from hard and variable stops, and adapts to longer-term trends in its positioning allows us to be relatively agnostic against the direction in which Bitcoin moves over time.

It does not matter whether Bitcoin succeeds or fails, as long as it continues to create unprecedented volatility.

Bitcoin May Enter Another Consolidation or Downtrend:

Recently, Bitcoin has entered a dangerous territory after the launch of the ICE Bakkt Futures – the first Bitcoin settled futures available to wall street institutions and retail brokerages. While it lingers in the 8000’s, it risks the possibility of a larger reversal akin to its former market cycle tops. Historically, Bitcoin has never closed below the 21 Simple Weekly moving average during a bull market. The moving average is a statistically significant mean reversion area that is programmed to be bought in Laissez-Faire, and has been an area of support over 20 times in Bitcoin’s history. More simply said, the odds are that Bitcoin’s price stays above this moving average; however, if this week ends with Bitcoin below $9000 that will be the first warning sign of a downtrend, and Laissez-Faire will begin to ‘adapt’ to the new market. Fundamentally speaking, I’d like to go into the economics of the situation and introduce a new model for Bitcoin pricing. As I’ve discussed before, Bitcoin miners ultimately run the market because they determine the circulating supply, and are the only means of creating new coins. Below is my theory from 2018 of how the market would operate according to miner economics.

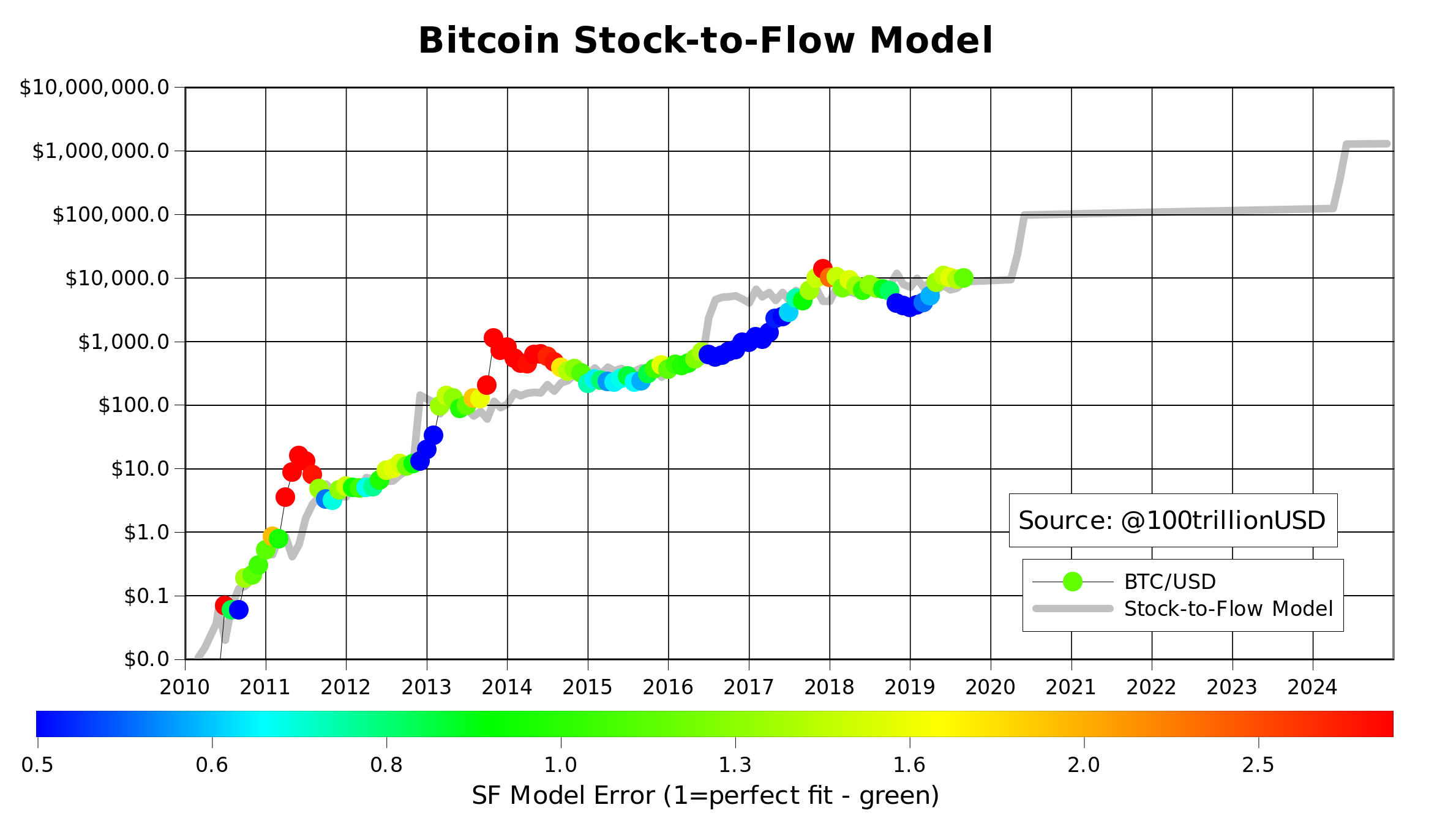

To summarize, Bitcoin’s market cycles act like many commodities affected by shortages and surpluses. Coffee, natural gas, grains, oil, etc. are all great examples of markets that ebb and flow with supply and demand, shortages and surpluses. Bitcoin is no exception, and no doubt the price is greatly influenced by its producers, the miners. While entering into the 7000’s and even 6000’s could be technically dangerous for Bitcoin – as long as the price is above the cost of production at the next halving in May 2020 there will likely be explosive results. In theory, that price would be around $8000-$9000. Let this be a segue into a very interesting price model for Bitcoin, the Stock to Flow Model. (Credit to the author, PlanB – 100trillionUSD)

First, we need to understand what Stock-to-Flow is.

Stock-to-flow Ratio:

Stock-to-flow Ratio for a commodity is defined as it’s years of inventory relative to annual supply. While the economic utility of a consumable good is created when it is destroyed or used up, the utility of investment assets lies in their possession and later resale. Industrial commodities, therefore, have low stock-to-flow ratios, this is to say, inventories usually only cover consumption demand for a few months. If there were no inventories at all, supply would have to correspond exactly to production and demand exactly to consumption. However, if there are inventories, consumption can temporarily exceed production. Since inventories of consumable commodities are as a rule very low, prices will rise quickly in anticipation of a future supply shortage and bring consumption into balance with production. As opposed to this, the price stability that comes with having a huge pile of inventory gives platinum, gold, and silver a new monetary aspect. The demand is driven by the store-of-value use case for gold, for instance, far outstrips that from actual industrial use cases. It’s apparent a similar store-of-value case can also be applied to Bitcoin.

The Stock-to-Flow Model is a useful way of determining the fair value or price discovery in Bitcoin and other commodities in that the more the price of the asset deviates from the stock-to-flow; the more it can be deemed undervalued or overvalued. It also can be used to estimate the future price of Bitcoin as long as we were to assume it would continue to obey the economics of the miners, the halving, and its inherent scarcity. Of course, the halving directly ties into this model as it immediately will affect the supply economics of Bitcoin. Read the prior article on the halving if you’d like to understand the implications of it more here. Interestingly enough, as of yesterday Bitcoin came into the area of stock-to-flow at $8,300.

Global Recession as a Threat or a Boon:

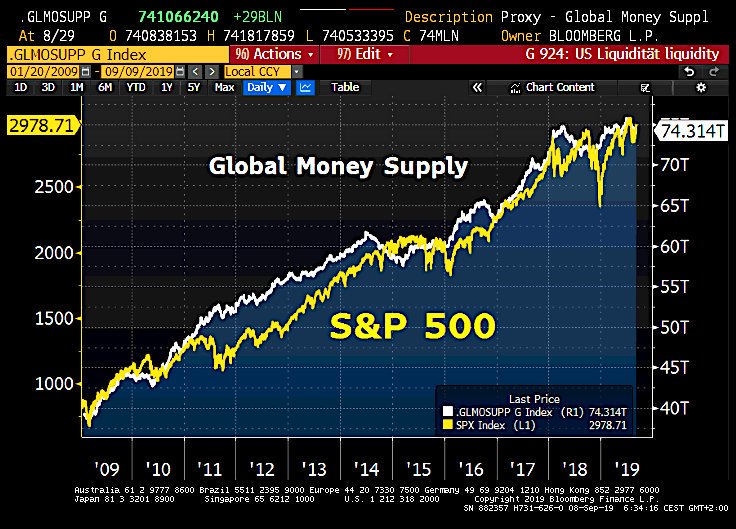

One looming uncertainty is the fact that Bitcoin has never endured a global recession, like 2008. Although many argue it was created as a response to it, that alone is not proper evidence that a recession would be inherently good for the price of Bitcoin. A lot of characteristics of the cryptocurrency demonstrate concepts of trust-less banking, sound and scarce money, and a step away from our current banking system which obviously failed during 2008. This creates a sort of counter ideology in which Bitcoin is the antithesis to greedy bankers and traditional markets. Many people in the space believe that Bitcoin is the ultimate answer to the central banking failures of inflation, soundless money backed by nothing, and even economic crisis. Bitcoin could change the world by creating a proof-of-work money that is backed by mathematics, decentralization, and value via scarcity. Many of these people argue that there is nothing scarce about the unlimited amount of USD, EUR, GBP, JPY, etc that can be printed; and they may be right. Below is the Bloomberg terminal Global Money Supply index compared to the Sp500.

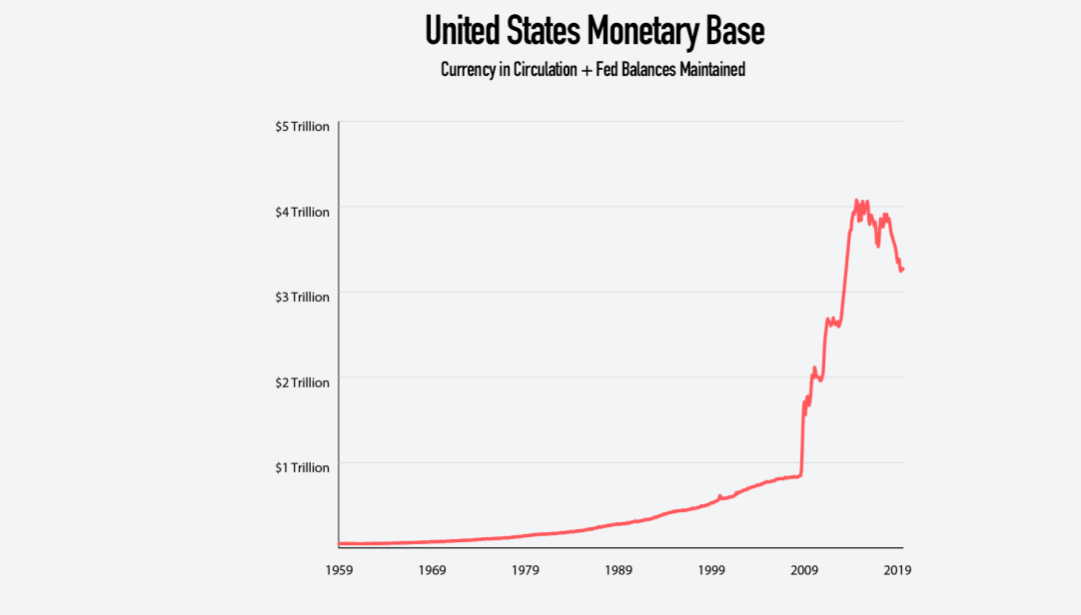

..and the United States Monetary Base since the 1950’s.

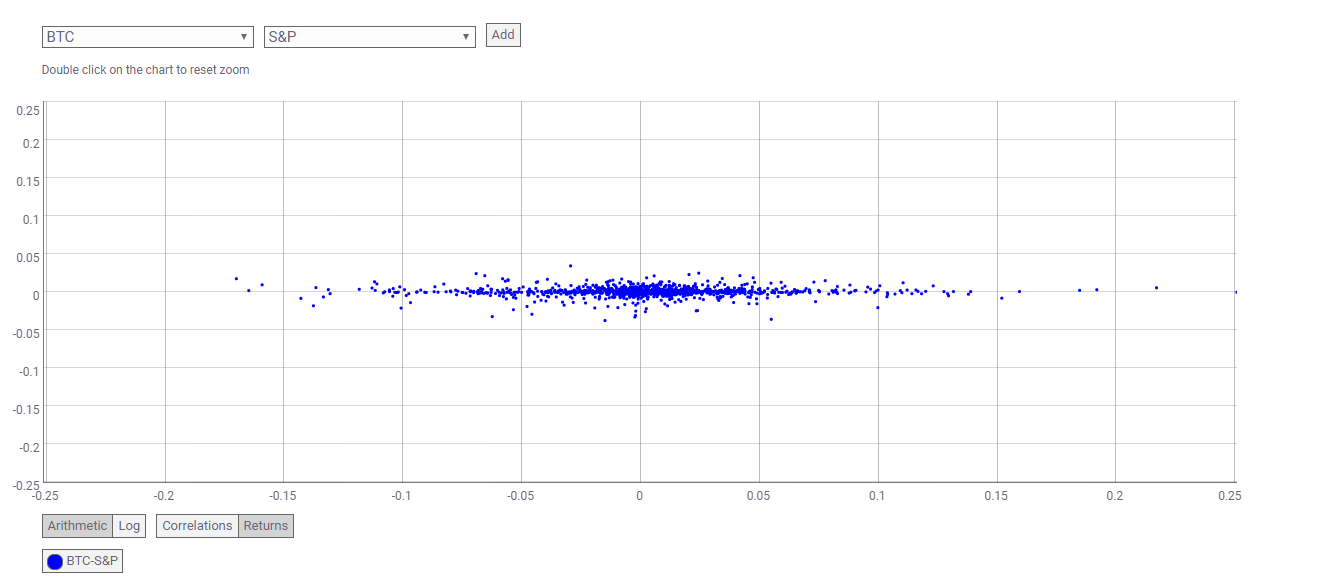

However, in my opinion, Bitcoin is nowhere close to that Utopian idealogue of a “global reserve asset”. Right now as evidenced by the markets; Bitcoin performs like a risk-on asset not unlike the traditional stock market. This is likely because institutions and individuals buy Bitcoin due to a surplus of wealth, speculative mentality, and general appetite for volatility and risk. When the world is ending like it was in 2008 and people are losing their homes, will they really be buying Bitcoin? If we look at the correlation of Bitcoin to the stock market it’s very apparent that more or less move together. This is further evidenced by them crashing and bottoming together in February 2018, November 2018, and them peaking together January 2017.

In conclusion, it’s likely Laissez-Faire will not only outperform the stock market but also Bitcoin during the next recession.

This market is really at a technological crossroad that will likely impact the future of the world, and it’s both exciting and fearsome. Cheers to a 100% return, very few draw-downs, a bit of luck, and some great people! I’m looking forward always to what this will become.

1 Comment found

Jason Johnson

Brilliant analysis and we shall be investing in Bitcoin.